Home Insurance in Missouri

When folks ask me at Hereth Insurance Consulting why home insurance in Missouri costs what it does, I usually tell them to picture the Show-Me State the way an underwriter does — sunny one afternoon, getting pounded by hail the next. Companies like Chubb, Amica, USAA, Allstate, The Hartford, Kin, and FSCB all price their policies around that unpredictability, whether your roof sits in the Ozarks, the Bootheel, or somewhere closer to Kansas City, St. Louis, Springfield, Independence, or Columbia. A solid homeowners insurance policy isn’t just paperwork; it’s the financial backbone that keeps a bad storm from becoming a bad decade.

Dwelling coverage sits at the center of nearly every quote I review, and the number attached to it — say $1,440 for $350,000 in protection — tells you a lot about how insurers weigh tornadoes, severe storms, and other natural disasters against your premium. What changes that number more than people expect is the boring stuff: your deductible, your credit, and your claims history. I’ve sat across the table from homeowners near the Tornado Alley corridor who assumed their rate was set in stone, only to learn that mortgage lenders, hailstorms, flooding risk along the Missouri River and Mississippi River, and even local construction costs were quietly doing the math behind the scenes.

Missouri has logged roughly 120 severe weather events causing billions in losses since 1980 — that’s not a scare tactic, it’s the reason underwriting practices in this state look different from neighboring ones. Policies here exist to deliver peace of mind and financial protection against fire, theft, and liability claims, and to cover temporary living expenses if a covered loss leaves your place uninhabitable.

I always remind clients that your home’s age, condition, and building materials matter just as much as the coverage amount you pick. Rebuilding isn’t about what you’d sell the house for; it’s about what it costs to put it back together. Life throws unpredictable moments at every resident, and homeowner or not, having the right policy in place is what keeps you in good hands when the sky turns green.

Is Home Insurance Required in Missouri?

Here’s something that surprises a lot of people I talk to: Missouri law doesn’t actually force anyone to carry homeowners insurance. If you’ve paid off your house and own it outright, you’re technically free to skip it. But the moment a mortgage enters the picture, your lender will almost certainly mandate coverage as a condition of the loan — and mortgage lenders aren’t being difficult, they’re protecting the asset tied to your finance agreement.

Even without that requirement, I’d argue it’s one of the worst places to go insured-free. There’s no one-size-fits-all policy that works for every situation; coverage should be tailored to your specific needs, your home’s quirks, and your risk tolerance. Given how frequently severe weather touches down across the state, going without protection in Missouri isn’t really optional in any practical sense, even if it’s not legally required on paper.

Standard/Typical Homeowners Insurance Coverages in Missouri

Most policies break down into the same core pieces, just labeled differently by each carrier. Dwelling coverage protects your roof, walls, flooring, and staircases — basically the bones of the house. Personal property coverage handles your furniture, clothing, and electronics, even if something’s stolen while you’re out and about. Other structures coverage steps in for a detached garage, fence, or shed sitting separate from the main build, and liability protection defends you if someone decides to sue after getting injured on your property or after you cause property damage to theirs.

Then there’s guest medical protection, which I think gets overlooked constantly — it covers medical expenses if a guest slips and sprains an ankle on your steps, regardless of whether you’re legally responsible. Additional living expenses protection (sometimes called loss of use coverage) pays for hotel expenses if a covered loss makes the house unfit to live in. Some carriers label these Coverage A through Coverage F: dwelling, other structures, personal property, loss of use, personal liability, and medical payments to others — the last of which covers accidentally hurt visitors but excludes your own household.

A feature like The Hartford’s ProtectorPLUS Zero Deductible Benefit can waive up to $5,000 off your base policy deductible once your total covered damages exceed $32,900 — the kind of detail clients rarely ask about until it saves them real money. Every one of these sits under a policy limit, a deductible, and a set of exclusions — read those carefully. Depending on your situation, you might also be shopping for renters insurance, condo insurance, mobile home insurance, scheduled property insurance, landlords insurance, or in-home business insurance instead of a standard homeowner policy, plus protection for jewelry, art, and collectibles that typically only get covered up to a specific limit.

Additional/Optional Coverages

This is where I spend most of my consulting time, honestly, because optional coverages are where real protection gaps get closed. Water back up coverage and sump pump overflow endorsements address water backup issues that standard policies exclude — though they still won’t touch damage from surface water or normal wear and tear. Building codes and service lines endorsements matter more than people assume, especially in older neighborhoods.

Full replacement cost coverage can push your payout up to 125% of your coverage limits for a total loss here in Missouri. Identity fraud expense coverage helps with out-of-pocket expenses tied to fraud or identity theft, while personal injury liability coverage covers a libel or slander claim — not something most homeowners think about until they need it. Reimbursement for replacing locks pays up to $500 with a $100 deductible if your keys go missing, and “new for old” protection replaces destroyed items with brand new equivalents instead of depreciated ones.

Equipment breakdown coverage handles mechanical breakdown or electrical breakdown in appliances and heating systems, and even sweetens the deal for green upgrades toward energy efficient or environmentally friendly replacements. The disappearing property deductible quietly shrinks your deductible after three consecutive years without an insurance loss. Amica’s endorsement list adds special computer coverage for desktops, laptops, smartphones, gaming devices, and smart TVs against accidental damage or theft, plus scheduled personal property for high-value items and fine art, and an earthquakes endorsement for earth movement damage.

Standard policies simply don’t touch floods — you’d need a separate flood insurance policy or National Flood Insurance Program coverage, especially if your address sits inside a floodplain. Locally, tornado/wind coverage often comes with a higher deductible if you’re in a zone with frequent tornadic activity, and hail coverage protects siding in places like St. Louis County, which carries a notably high risk index. Sump pump and sewage back-up issues from heavy storms need their own water back-up coverage, and if you want broader liability protection for your assets, an umbrella policy is worth the conversation.

Earthquake Coverage in Missouri

Most people I talk to are shocked to learn small earthquakes happen in Missouri almost every day, according to the Missouri Department of Natural Resources. Standard homeowners insurance excludes damage from earth movement, including full-blown earthquake events, so your policy simply won’t help if a tremor cracks your foundation. The fix is a dedicated endorsement that extends coverage specifically for earthquake damage — cheap insurance against a risk most homeowners don’t realize they’re carrying.

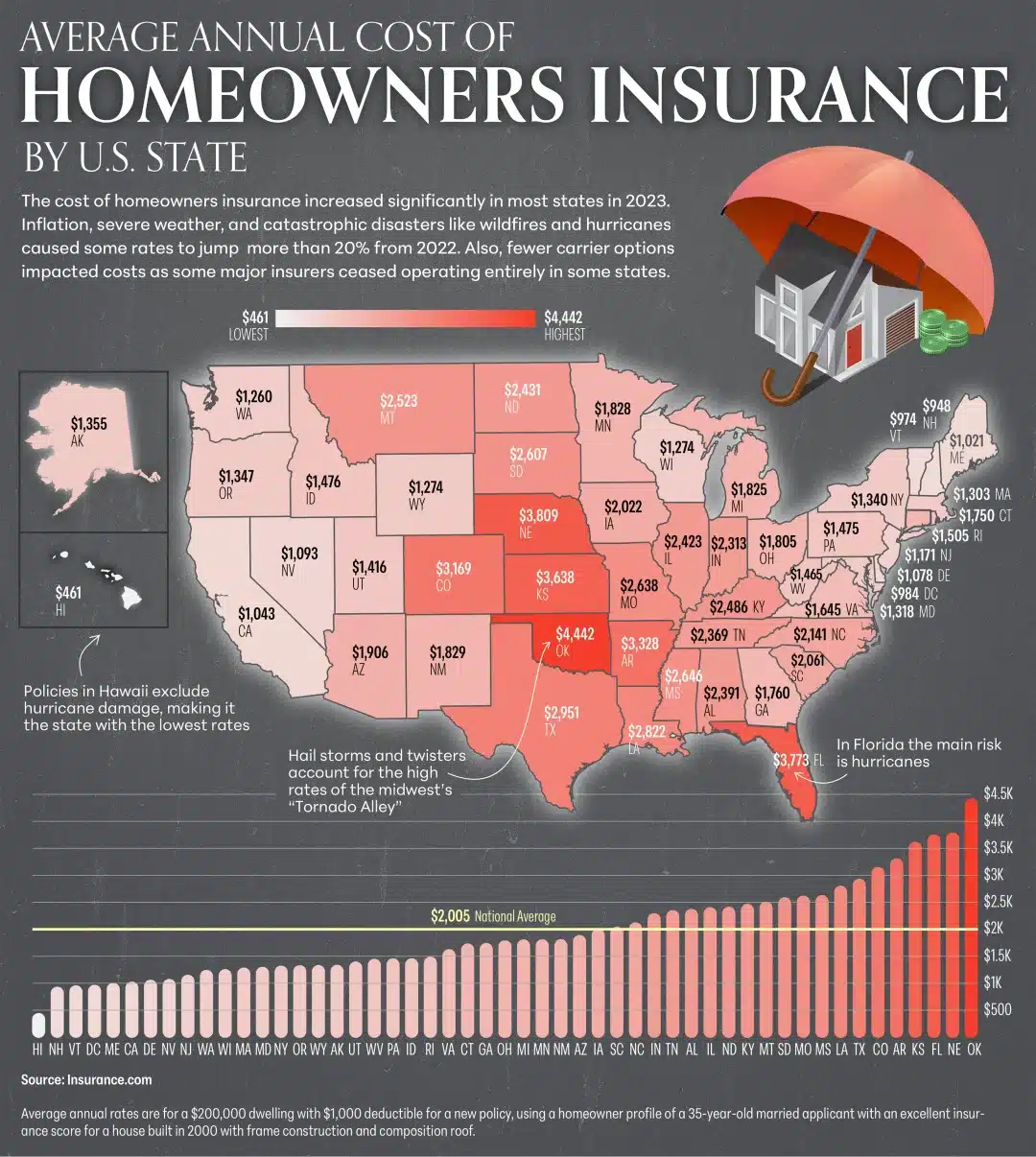

Average Cost of Home Insurance in Missouri

Numbers tell the real story here. Missouri homeowners pay around $3,805 annually, or about $317 monthly — a striking 53% above the national average of $2,490 for comparable dwelling coverage at $400,000, paired with $300,000 in liability coverage, a $1,000 deductible, and no recent claims. The rebuilding cost behind these numbers — driven by labor and construction pricing — lands around $363,286 in Missouri according to First Street, a respected climate risk modeling firm.

Coverage limits have a major impact on Missouri home insurance costs, with premiums ranging from about $2,100 for $200,000 in coverage up through $3,805 for $400,000, and reaching roughly $5,455 for $600,000. Homeowners with poor credit may pay as much as $7,715 annually — over 100% more than those with good credit.

While Missouri’s overall home insurance costs have climbed above the national average in recent years due to increasingly frequent severe weather, rates still vary significantly by location, home size, and coverage level. Coverage limits play a key role in determining both rebuilding protection and personal property coverage, while the state’s frequent severe weather events continue to drive insurance costs higher year over year.

Cost by Region/Area

Location genuinely changes everything here, mostly because of regional weather patterns. Eastern Missouri, especially near St. Louis, deals with flooding risk from the Mississippi River, plus tornadoes and hail — which is why it ranks highest in relative cost. Western Missouri, closer to Kansas City and brushing up against Tornado Alley, sees above average pricing thanks to wind damage from storms and frequent thunderstorms. Central Missouri sits at moderate cost, dealing mainly with hail and windstorms, while the southern Missouri Ozarks region is the most affordable, even with occasional flash flooding.

For homeowners stuck in high-risk areas who can’t find coverage through the standard insurance market because of repeated natural disasters, the Missouri Property Insurance Placement Facility — known locally as the FAIR Plan — offers basic home insurance when private insurers say no. As a state-mandated program and market of last resort, it requires proof you’ve been denied coverage elsewhere, and the trade-off is limited coverage at higher rates.

Factors That Impact the Cost of Home Insurance in Missouri

Every insurer weighs multiple factors differently, but a few show up constantly in my conversations with clients. Location alone is a major factor — premiums shift based on local risks and exposures, whether you’re in a city or small town, and how close you sit to emergency services like a fire station. The age of your home and construction costs to fix it matter just as much; your residence should have tailored, customized coverage that gets reviewed and updated regularly rather than left on autopilot.

Pricing policies also weighs your ZIP code against known weather risks — tornadoes, severe thunderstorms, hailstorms, and proximity to rivers all push flooding risks higher. Roofs, plumbing, and electrical systems age right along with the house, and older versions of any of those raise the odds of a peril-triggered claim. Roof type and hail resistance specifically matter in a state where hail damage is common — newer roofs built to resist wind and siding damage can earn lower premiums, especially around St. Louis County’s elevated risk index for tornado damage and tornadic activity.

Your own claims history factors in too — multiple claims can flag you as a higher-risk customer. And behind the scenes, insurers are managing their own reinsurance costs, the price they pay to protect themselves from massive losses after major disasters — costs that eventually filter down to policyholders like you.

Discounts / How to Save on Home Insurance in Missouri

Saving money on coverage isn’t complicated, but it does take some legwork. Multi-policy discounts from carriers like Allstate reward you for bundling home insurance with auto insurance, and a responsible payer discount kicks in for payment methods like in-full payment or escrow, plus a clean payment history of paying on time. A claim-free discount rewards switching carriers without a recent claim, and claim forgiveness keeps your rate from jumping just because you filed one.

The Hartford offers 12% off car insurance and 20% off MO homeowners insurance when you bundle, saving customers an average of $963. My advice always starts the same way: shop around for quotes from multiple insurance companies, research their insurance ratings and what actual customers say, review policy details and coverage levels carefully, and ask directly about discount opportunities tied to bundling.

Amica offers savings for alarm systems — burglar alarms, sprinkler systems, fire alarms — and for automatic detection devices like temperature monitoring, water leak detection, or gas leak detection. A new or remodeled home earns a credit, staying claim-free for three years earns a discount, and simple steps like AutoPay (automatic deductions) or signing up for e-discount billing electronically add up. Bundling insurance, especially with Amica, can mean a multiline discount worth 20%, and you’re not limited to car insurance — bundling extends to boat, RV, life, and umbrella insurance too.

Beyond bundling, increasing your deductible lowers premiums but raises what you pay out of pocket per claim. Strengthening your home with impact-resistant roofing, reinforced garage doors, and storm shutters — what the industry calls home hardening — can unlock real discounts. Security systems, smoke detectors, and burglar alarms help too, and replacing aging systems like plumbing, HVAC, and electrical systems reduces risk while lowering your premium. In short: bundling policies, installing alarm systems and safety devices, and making home upgrades are the three levers I tell clients to pull first.

How to Get Home Insurance in Missouri

Getting covered properly starts with choosing your coverage alongside an agent who can help design a policy that actually fits your place — no two homes are identical, so this shouldn’t be a copy-paste exercise. From there, you apply for a policy, and a good carrier makes that process quick and easy so you’re protecting your home without unnecessary delay. As your life changes, your insurance needs should evolve with it, which is why staying protected means revisiting your policy periodically, not just signing once and forgetting about it.

At a place like Amica, the path looks like three steps: an Amica representative helps assess your coverage needs with personalized guidance, helping you navigate options suited to your situation; next, they help you discover potential discounts and other cost-saving measures based on your unique circumstances; finally, you get a quote — either a home insurance quote online or by calling to speak with a representative directly.

Best Home Insurance Companies in Missouri (Ratings/Reviews)

Chubb earns its reputation for best coverage on high-value homes, built for affluent homeowners who want generous coverage and high limits. Its HomeScan feature uses infrared technology to spot leaks behind walls before they become disasters, and a cash settlement option exists if you’d rather not rebuild. It posts far fewer consumer complaints than expected, bundles standard coverage that’s usually sold as extras elsewhere, and offers genuine perks — though most people can’t get a quote online and need a local agent.

Amica wins on best digital tools, letting you manage your policy, pay bills, and file claims online, backed by live chat representatives available seven days a week. Its Platinum Choice Home package adds coverage for valuable belongings, and strong customer satisfaction ratings come paired with dividend policies that return part of your premiums — though the buying process sometimes finishes over the phone rather than fully online.

State Farm takes best value, with low rates and generous discounts — bundling can save over $1,000, and Missouri policyholders get a free Ting device that monitors your electrical system to help prevent fires. Its user-friendly website and personalized service are strong points, structural coverage tends to be generous, though a recent J.D. Power study flagged below-average claim satisfaction. Rates run $2,050 (for $200K coverage), $2,600 ($300K), $3,065 ($400K), $3,465 ($500K), and $3,855 ($600K).

Cincinnati Insurance claims fewest complaints, with notably low consumer complaints and a nice discount for water shutoff devices that catch a leak before it spreads. It offers various coverage options for higher-value homes, though there are no online quotes — everything runs through independent agents.

USAA is the clear pick for military families — active military, veterans, federal workers, and their families get deductible-free coverage for military uniforms and equipment, plus home-sharing or landlord coverage for those deployed. Its replacement cost basis means brand-new replacements instead of depreciated payouts, with rates of $1,065 ($200K coverage), $1,370 ($300K), $1,635 ($400K), $1,885 ($500K), and $2,115 ($600K).

Rounding out the field: Country Financial holds a 4.6 rating, Allstate earns 4.5 with an average rate near $3,790, and Openly also sits at 4.5 — all worth a look based on their NerdWallet rating and overall star rating.

Facts and Figures About Missouri (Common Claims & Fun Facts)

Missouri’s diverse climate throws a lot of different weather conditions at homeowners throughout the year. Frozen pipes are a classic cold-weather claim — when temperatures drop below freezing, water pipes can burst, causing serious water damage; as long as heat was properly maintained in the home, burst pipes damage including water cleanup and repairs is typically covered. Weather-related claims cover a lot of ground too: tornadoes, high winds, and hail routinely cause roof damage, siding damage, and water intrusion, and standard coverage generally extends to windstorms, lightning, and other weather-related perils.

On a lighter note, Missouri is home to nearly 90,000 farms, with 90% of them family owned — a detail I love sharing with clients who’ve just moved from out of state. St. Louis hosts the iconic Gateway Arch, a symbol of westward expansion, and the state holds over 7,000 caves, giving it one of the highest number of caves anywhere in the country.

Inventorying Your Rooms & Property

This is the step almost everyone skips, and it’s the one I push hardest in client meetings. Your home inventory should get a review and update once a year, capturing every piece of personal property with real details. Missouri’s own home inventory checklist makes it easier — start by jotting down notes on everything you own, staying as detailed as possible.

Don’t try to tackle the whole house at once: choose one room first, then move room by room to keep things manageable. Record specifics for each item — serial numbers, model numbers, purchase date, and price — and take photos so you have proof of condition before any damages ever happen.

Frequently Asked Questions

What does home insurance in Missouri typically cover?

Home insurance in Missouri generally covers your dwelling, personal property, liability protection, and additional living expenses if your home becomes uninhabitable due to covered events like fire or storms.

Why is home insurance in Missouri more expensive in some areas?

In Missouri, premiums vary because of tornado risk, hail damage frequency, flood exposure, crime rates, and rebuilding costs that differ by city and ZIP code.

Is home insurance required in Missouri?

Home insurance is not legally required in Missouri, but mortgage lenders usually require it to protect the property until the loan is fully paid.

What are the most common risks covered in Missouri home insurance?

Typical risks include fire, windstorms, hail, lightning, theft, and certain water damage scenarios, though flood and earthquake coverage often require separate policies.

How much does home insurance cost in Missouri on average?

Costs vary widely, but Missouri homeowners typically pay around or slightly above the national average due to severe weather exposure and regional risk factors.

Does Missouri home insurance cover tornado damage?

Yes, most standard home insurance policies in Missouri cover tornado damage under windstorm protection, but deductibles may be higher in high-risk zones.

How can I lower my home insurance premium in Missouri?

You can reduce costs by bundling policies, increasing deductibles, installing safety systems, maintaining a claims-free history, and comparing multiple insurance providers.

Which factors affect home insurance rates in Missouri the most?

Key factors include home location, age of the property, construction type, credit history (where applicable), coverage limits, and the insurer’s risk model.